Spring has sprung and summer is on its way! This time of year makes many want to get their golf clubs out and hit the golf course. As you may know, golf can become addicting no matter how great or how “not so great” your game may be. As a financial professional you probably find little time to enjoy a golf game, and would love the opportunity to be on the course a little more often. Have you thought of using golf as a client appreciation event? The truth is that if you don’t appreciate your clients, someone else will.

Read More

Tags:

prospecting,

marketing for independent agents,

retirement strategies

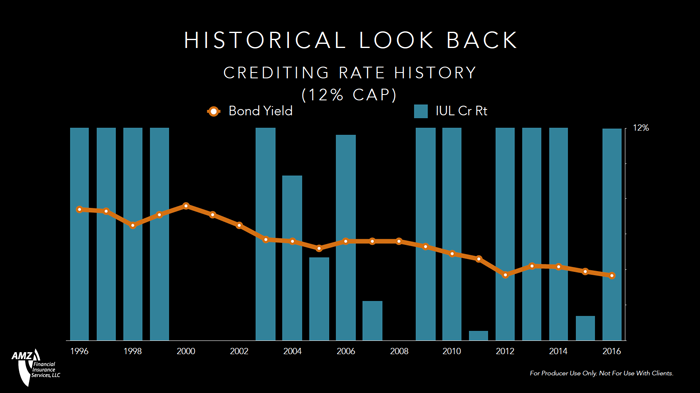

A very basic way to understand how Indexed Universal Life (IUL) credits interest is to think of it like a very simple game where you flip a coin 10 times. There are then two ways to play the game. In Game 1 you win $100 for every head, and lose $100 for every tail. Game 2 awards you $70 for every head, but you lose nothing for every tail.

Read More

Tags:

IUL (indexed universal life insurance),

retirement strategies

Every client has different goals and resources as they prepare for retirement. There are five important details to consider when working with clients. These are not the only necessary details required for helping clients plan for retirement, but they should not be overlooked.

Read More

Tags:

coaching,

retirement strategies

A basic principle of investing is that you should gradually reduce your exposure to risk as you get older. Generally speaking, a younger investor has a longer time horizon and therefore can absorb more short-term investment risk. An older investor has a shorter time horizon and therefore doesn’t have as much time to absorb short-term investment risk.

Read More

Tags:

coaching,

retirement strategies

Today with so many carriers and marketing organizations jumping on the Indexed Universal Life (IUL) bandwagon, it’s hard to believe that the product was actually introduced to the market in 1997. Back then, forward-looking insurance companies were trying to find ways to make their fixed insurance products more attractive.

Read More

Tags:

IUL (indexed universal life insurance),

retirement strategies

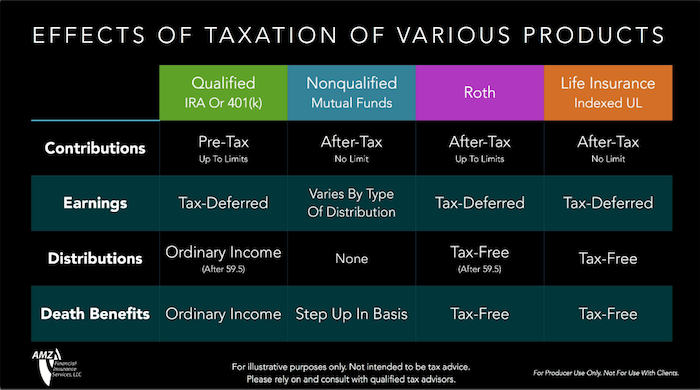

When choosing the best financial product for your clients, you must take the tax advantages or disadvantages into account. The way contributions, earnings, distributions, and death benefits are taxed could dramatically impact how much your clients or their beneficiaries receive when their accounts are cashed out. Here's a high level comparison of how taxes impact your clients' different financial accounts.

Read More

Tags:

IUL (indexed universal life insurance),

taxes,

retirement strategies

Case design and illustration requests are common daily events that Independent Marketing Organizations (IMOs) handle for advisors they work with. Many of the advisors we work with do a great job of fact finding during the first meeting with a client. Getting the facts and details up-front are extremely important for putting together a good, strong recommendation that can be presented during your next meeting.

Read More

Tags:

coaching,

retirement strategies

Are you a financial services supplier or an architect? Your clients may be viewing you as one or the other. When it comes to building homes (or financial plans) the raw material supplier and the architect both play a significant role in the construction of a home. Neither is necessarily bad or good, better or worse. They have very different roles to play, and they have very different perspectives.

Read More

Tags:

prospecting,

coaching,

retirement strategies

Every home needs a solid foundation. The same holds true for financial plans. When it comes to constructing a new home, one of the first crews on sight is the excavation team. They dig and lay the foundation. The foundation determines the long-term stability of the home to be built on top of it.

Read More

Tags:

coaching,

retirement strategies

When it comes to wealth management, your client's money can do two things: It can earn interest or buy stuff. The problem is that many clients have "lazy money" just sitting around waiting to be spent. Money gets "lazy" when it is not being used to do one of the two things it can do with respect to wealth management.

Read More

Tags:

retirement strategies