One of the most common risks in retirement is order of returns risk (also known as: sequence of returns risk). It is well known within the financial services industry that investing in marketable securities exposes clients to this risk. However, do your clients know that many indexed products are not immune from order of returns risk?

A product whose future value is unknown, and relative to a variable interest rate or market-based rate of return, is exposed to this phenomenon. Order of returns risk is the chance that the value of the account might go up (+) or down (-) in any given year. Real world market based returns don’t occur in a straight-line pattern and market predictions can never be certain.

Uncommon Knowledge of a Common Risk

Most clients understand that if they own stocks, bonds, or mutual funds within their retirement accounts, the value of their acocunts today is probably different than five years ago, and will likely be different five years from now. As clients are accumulating resources for retirement or just beginning to pay for retirement expenses, the order of returns can significantly effect their account values.

More Money Equals Greater Effect

The impact for clients near retirement will most likely be magnified because the value of their accounts are probably larger than they were the day they made their first deposits. If your client's first deposit was $1000, and the market moved up by 10%, their deposit is now worth $1,100. That’s a $100 change. However, as your client nears retirement their account might be worth $500,000. A 10% increase is equal to a $50,000 change. The monetary impact of the return is magnified by the size of the total account.

Losses are also magnified. Imagine if your client retired with $500,000 invested just before the market experienced a 20% correction. The client's $500,000 would drop to $400,000. If they didn't need any of this money to replace their paycheck post retirement, they could be patient and wait for the market to come back.

Bonus Question: What rate of return is needed to get back to even?

25% ($400,000 X 1.25 = $500,000). They would need a much greater return than their loss for the account to get back to its starting value.

Stepping On The Accelerator

The option to wait for positive returns to accumulate and offset a large loss is not available for many clients. Imagine your client's household needs $25,000 (5% of $500,000) annually to supplement their income. Forced into taking around a 27% loss, their investment now becomes $346,275. A return of over 44% is needed the following year to get back to $500,000.

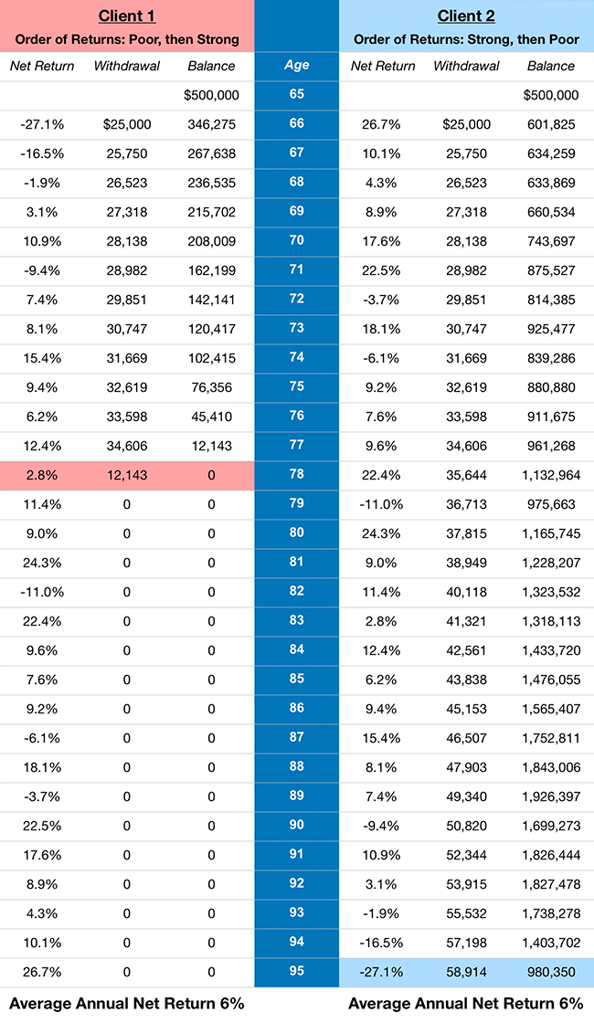

The chart below demonstrates how the order of returns effects the outcome of a $500,000 account balance for two clients who both average a 6% rate of return while withdrawing 5% annually adjusted for inflation to supplement their retirement income. Client 1 experiences an adverse order of returns, poor returns followed by strong returns, and runs out early. Client 2 experiences a favorable order of returns, strong returns followed by poor returns, and lives in abundance.

Fixed Index Products Are Exposed Too

Although there may be protection from negative market returns, an indexed annuity may experience a zero year. If you’ve added a rider, such as a guaranteed income feature at an additional cost, the product is effected by the order of interest credits experienced. However this strategy can reduce the negative impact of order of returns risk.

With indexed universal life insurance (IUL), a zero year is also a possibility, since there are "floors" that protect the account from negative index performance. Internal policy fees and charges are still applicable even in a year when there are no interest credits. A year with zero interest credits, less fees and charges, is a possible outcome.

Risk Zone

The 10 years prior to retirement and the 10 years after retirement is when your clients may be most susceptible to this retirement risk. During this time, an adverse order of returns could accelerate the pace at which they draw down their retirement resources.

Order of returns risk is manageable. In some cases, it may be mitigated or even eliminated all together through proper planning. Have an open discussion with your clients about exposure to order of returns risk. Draft a written retirement plan that deals with this risk so each of your clients can avoid taking a significant loss during a down market and enjoy their retirement.